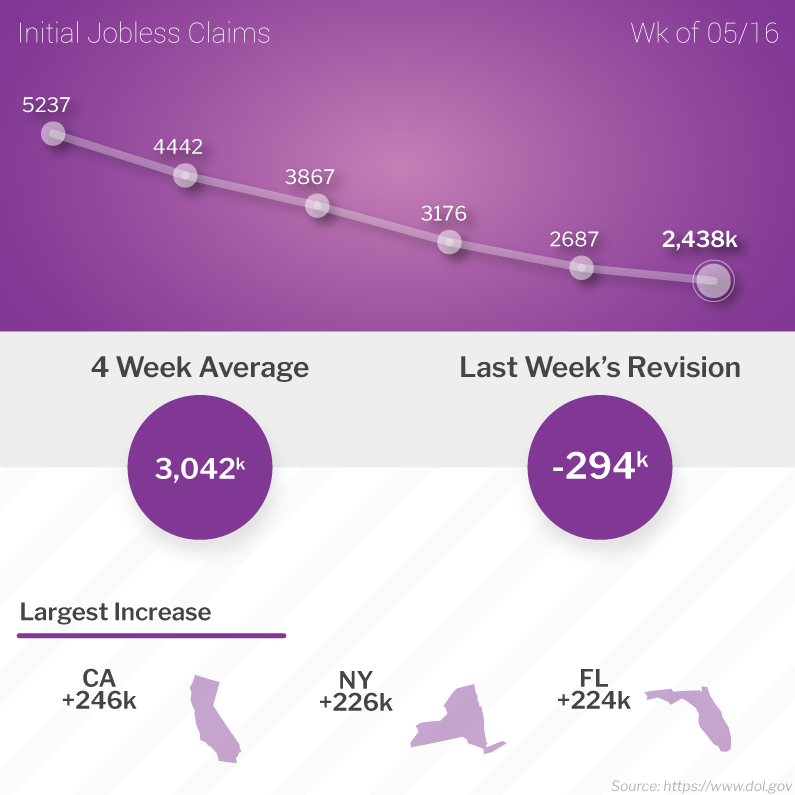

Professionals around the country continue to feel the lasting impact of the COVID-19 pandemic, as another 2.44 million people filed for unemployment during the week ending May 16.

In housing news, the National Association of Home Builders released its Housing Market Index, which is a real-time read on builder confidence. While all components improved from April to May, the figures are still understandably and significantly lower than they were in March.

Reports also showed that Housing Starts and Building Permits both plunged from March to April, as did sales of existing homes.

In housing news, the National Association of Home Builders released its Housing Market Index, which is a real-time read on builder confidence. While all components improved from April to May, the figures are still understandably and significantly lower than they were in March.

Reports also showed that Housing Starts and Building Permits both plunged from March to April, as did sales of existing homes.

Fed chair Jerome Powell was in the news, appearing on 60 Minutes and testifying in front of the Senate. Of note, he said on 60 Minutes that the economy could shrink upwards of 30% in the second quarter. However, he does not see the economy entering another depression and he believes the US will get to “an even better place” than it was before the coronavirus hit, and that it “won’t take that long.”

Lastly, there was some promising information at the start of the week from Moderna regarding its vaccine trials, as 45 participants produced COVID-19 antibodies. Stocks responded favorably when the news was first reported.

Unemployment Woes Continue

Another 2.44 million people filed for unemployment for the first time during the week ending May 16, which was in line with estimates. California (+246K), New York (+226K) and Florida (+224K) saw the largest gains.

Factoring in the number of new claims, continuing claims and the amount of people in the labor force, we estimate that the unemployment rate is around 21.5%. However, not counting new jobs the Paycheck Protection Program has temporarily created, we think that the unemployment rate could be closer to 24.7%.

Lastly, there was some promising information at the start of the week from Moderna regarding its vaccine trials, as 45 participants produced COVID-19 antibodies. Stocks responded favorably when the news was first reported.

Unemployment Woes Continue

Another 2.44 million people filed for unemployment for the first time during the week ending May 16, which was in line with estimates. California (+246K), New York (+226K) and Florida (+224K) saw the largest gains.

Factoring in the number of new claims, continuing claims and the amount of people in the labor force, we estimate that the unemployment rate is around 21.5%. However, not counting new jobs the Paycheck Protection Program has temporarily created, we think that the unemployment rate could be closer to 24.7%.

The latest Existing Home Sales report, which measures closings in April and likely represents buyers shopping for homes in February and March, showed that sales decreased by 17.8% from March to April. This was the largest monthly drop since July 2010 when the home buyer tax credit, a federal stimulus resulting from the subprime mortgage crash, expired. Sales were also 17.2% lower when compared to April of last year.

The median home price was reported at $286,800, up 7.4% year over year. Single family sales were down 16.9% compared to March, but condos saw a much bigger drop of 26.4%. This could start to show the migration from cities into suburbs.

Inventory was much tighter and remains a concern, as there were only 1.47 million units for sale in April, down 1.3% from March and a whopping 19.7% lower than last April.

At the current pace of sales, this represents a 4.1-month supply and is the lowest April supply figure on record.

As NAR's chief economist Lawrence Yun explained, “Record-low mortgage rates are likely to remain in place for the rest of the year and will be the key factor driving housing demand as state economies steadily reopen. Still, more listings and increased home construction will be needed to tame price growth."

And Speaking of Home Construction …

The Housing Market Index for the month of May increased to 37 from 30 in April, though it’s just over half the 72 reading that was reported in March.

Diving deeper into the survey's components, confidence in present conditions rose 6 points to 42 from April, versus 79 in March. Future expectations were up 10 points from April to 46, as compared with 75 in March, while prospective buyer traffic rose to 21 from 13 after reaching 56 in March. Anything above 50 signals expansion while below means contraction.

The NAHB said, "The fact that most states classified housing as an essential business during this crisis helped to keep many residential construction workers on the job." Also, "Low interest rates are helping to sustain demand."

The caveat, however, is that, "High unemployment and supply side challenges… are near term limiting factors."

Home construction figures were also released for April, with Housing Starts down 30% from March, the biggest percentage decline on record.

While we can likely expect housing to slow, the lack of supply as noted above will be supportive of home prices.

FHFA Update on Home Forbearance

The Federal Housing Finance Agency announced that Fannie Mae and Freddie Mac borrowers in forbearance can apply for refinancing and new purchase mortgages once their loans are current. The policy waives a previous mandatory wait of 12 months, which will allow faster access to record-low rates.

According to the FHFA, borrowers are eligible to refi or purchase a new home if they are current on their mortgage in forbearance but continued to make mortgage payments or reinstated their mortgage. Borrowers are eligible to refinance or buy a new home three months after their forbearance ends and they have made three consecutive payments under their repayment plan, payment deferral option or loan modification.

Said FHFA Director Mark Calabria. "Today's action allows homeowners to access record low mortgage rates and keeps the mortgage market functioning as efficiently as possible."

What to Look for This Week

After the Monday market closures in honor of the Memorial Day holiday, the rest of the week is jam-packed with reports. Tuesday including the Case-Shiller and FHFA home price indexes for March and New Home Sales for April, plus May Consumer Confidence.

April Durable Goods and the second estimate for 1Q GDP will provide important updates on the economy. Friday brings the final Consumer Sentiment numbers and manufacturing highlights via the Chicago PMI for May.

Technical Picture

The Fed continues to purchase Mortgage Backed Securities. After falling below support at the 50-day Moving Average at the start of the week, MBS were able to rally and now continue to trade in the middle of a 53bp range between the aforementioned support and overhead resistance at the 25-day Moving Average.

The 10-year is in a similar position, being squeezed in a range between its 25 and 50-day Moving Averages, though it has been moving lower and testing the 25-day. This is related to the negative stochastic crossover on the stochastic chart. If Treasury yields break beneath the 25-day, we may see Mortgage Bonds move higher and follow suit.

Source: Homebridge Financial Services

The median home price was reported at $286,800, up 7.4% year over year. Single family sales were down 16.9% compared to March, but condos saw a much bigger drop of 26.4%. This could start to show the migration from cities into suburbs.

Inventory was much tighter and remains a concern, as there were only 1.47 million units for sale in April, down 1.3% from March and a whopping 19.7% lower than last April.

At the current pace of sales, this represents a 4.1-month supply and is the lowest April supply figure on record.

As NAR's chief economist Lawrence Yun explained, “Record-low mortgage rates are likely to remain in place for the rest of the year and will be the key factor driving housing demand as state economies steadily reopen. Still, more listings and increased home construction will be needed to tame price growth."

And Speaking of Home Construction …

The Housing Market Index for the month of May increased to 37 from 30 in April, though it’s just over half the 72 reading that was reported in March.

Diving deeper into the survey's components, confidence in present conditions rose 6 points to 42 from April, versus 79 in March. Future expectations were up 10 points from April to 46, as compared with 75 in March, while prospective buyer traffic rose to 21 from 13 after reaching 56 in March. Anything above 50 signals expansion while below means contraction.

The NAHB said, "The fact that most states classified housing as an essential business during this crisis helped to keep many residential construction workers on the job." Also, "Low interest rates are helping to sustain demand."

The caveat, however, is that, "High unemployment and supply side challenges… are near term limiting factors."

Home construction figures were also released for April, with Housing Starts down 30% from March, the biggest percentage decline on record.

While we can likely expect housing to slow, the lack of supply as noted above will be supportive of home prices.

FHFA Update on Home Forbearance

The Federal Housing Finance Agency announced that Fannie Mae and Freddie Mac borrowers in forbearance can apply for refinancing and new purchase mortgages once their loans are current. The policy waives a previous mandatory wait of 12 months, which will allow faster access to record-low rates.

According to the FHFA, borrowers are eligible to refi or purchase a new home if they are current on their mortgage in forbearance but continued to make mortgage payments or reinstated their mortgage. Borrowers are eligible to refinance or buy a new home three months after their forbearance ends and they have made three consecutive payments under their repayment plan, payment deferral option or loan modification.

Said FHFA Director Mark Calabria. "Today's action allows homeowners to access record low mortgage rates and keeps the mortgage market functioning as efficiently as possible."

What to Look for This Week

After the Monday market closures in honor of the Memorial Day holiday, the rest of the week is jam-packed with reports. Tuesday including the Case-Shiller and FHFA home price indexes for March and New Home Sales for April, plus May Consumer Confidence.

April Durable Goods and the second estimate for 1Q GDP will provide important updates on the economy. Friday brings the final Consumer Sentiment numbers and manufacturing highlights via the Chicago PMI for May.

Technical Picture

The Fed continues to purchase Mortgage Backed Securities. After falling below support at the 50-day Moving Average at the start of the week, MBS were able to rally and now continue to trade in the middle of a 53bp range between the aforementioned support and overhead resistance at the 25-day Moving Average.

The 10-year is in a similar position, being squeezed in a range between its 25 and 50-day Moving Averages, though it has been moving lower and testing the 25-day. This is related to the negative stochastic crossover on the stochastic chart. If Treasury yields break beneath the 25-day, we may see Mortgage Bonds move higher and follow suit.

Source: Homebridge Financial Services

RSS Feed

RSS Feed